MRP glossary TOP > I > Internal Cost and External Cost

Internal Cost and External Cost

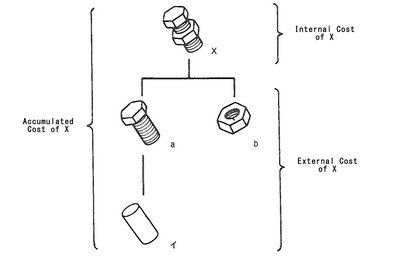

An item cost can be classified into its internal cost and external cost. Focusing on the cost of a certain item which is one component of a product, the cost is divided into two: the cost required to manufacture the item and the one required to process and purchase the assemblies of the item, or its child items. The former is called internal cost, and the latter is called external cost. Summing both costs are called accumulated cost of the item.

In the figure, Product X is assembled using assemblies a and b. In this case, the internal cost of Product X is the one required to assemble Product X, while the external cost is summing the processing cost of Assembly a, the purchasing cost of Part b, and the main material cost of material "イ" (the difference of each physical unit and failure rate is considered).

In addition, the accumulated cost of Product X is obtained by summing the internal cost and external cost.

In this way, by controlling the cost of each item with its internal and external costs, more detailed analysis of cost is possible and the influence caused by cost change can be easily grasped for its simple accumulation.

Related term: Cost Structure

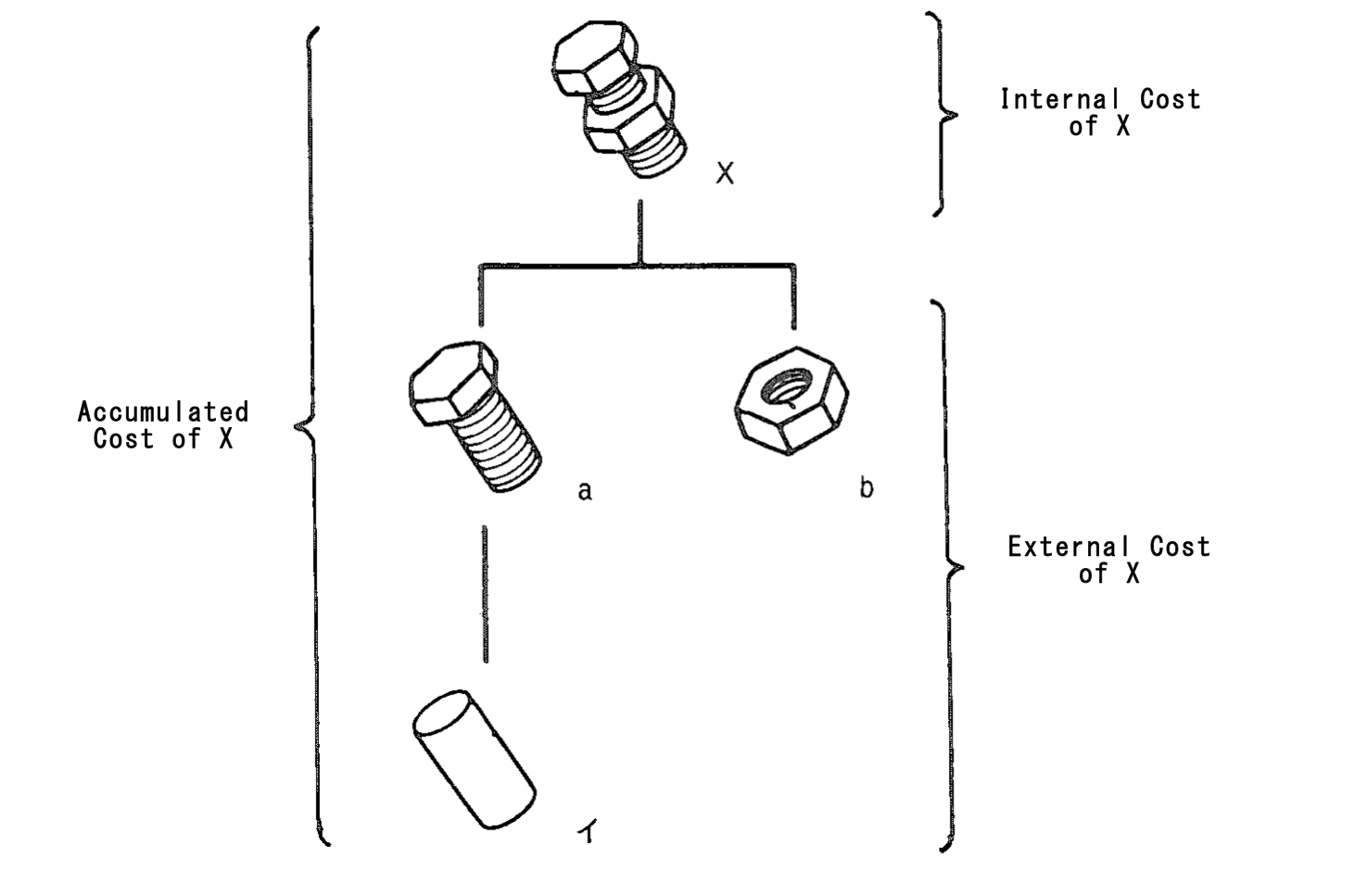

In the figure, Product X is assembled using assemblies a and b. In this case, the internal cost of Product X is the one required to assemble Product X, while the external cost is summing the processing cost of Assembly a, the purchasing cost of Part b, and the main material cost of material "イ" (the difference of each physical unit and failure rate is considered).

In addition, the accumulated cost of Product X is obtained by summing the internal cost and external cost.

In this way, by controlling the cost of each item with its internal and external costs, more detailed analysis of cost is possible and the influence caused by cost change can be easily grasped for its simple accumulation.

Related term: Cost Structure

Reference:JIT Business Research Mr. Hirano Hiroyuki