MRP glossary TOP > S > Standard Cost

Standard Cost

Standard Cost

It refers to the cost which is calculated in a scientific and statistical manner using the standard consumption amount and standard price, which can be an efficiency scale. This is an in-advance cost, and is also a substantial cost based on the standard situation.

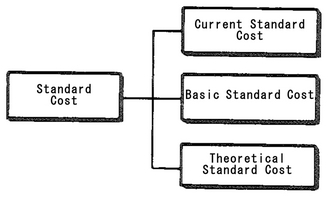

The standard cost has the following types:

Related term: Cost Structure

It refers to the cost which is calculated in a scientific and statistical manner using the standard consumption amount and standard price, which can be an efficiency scale. This is an in-advance cost, and is also a substantial cost based on the standard situation.

The standard cost has the following types:

- Current Standard Cost:

- It refers to the realistic standard cost, which shows an achievable cost goal considering normally-occurring spoilage, depletion, and loss rate like idle time. In addition, this standard cost is based on the actual situation, and when significant changes in material and labor costs occur within the same fiscal year, it is revised as needed and used as a base of budget or for the stocktaking valuation.

- Basic Standard Cost:

- It refers to normal standard cost, and once it is determined, the cost is continuously and subsequently used as a base in order to grasp the future cost trend.

- Theoretical Standard Cost:

- It refers to the ideal standard cost, which shows the lowest cost as a challenge calculated by theoretically achievable highest capacity utilization and the highest efficiency. In this case, the value obtained by subtracting the values of e.g. spoilage, depletion, and loss rate from the past value is used.

Related term: Cost Structure

Reference:JIT Business Research Mr. Hirano Hiroyuki