MRP glossary TOP > Cost Control > Cost Structure

Cost Structure

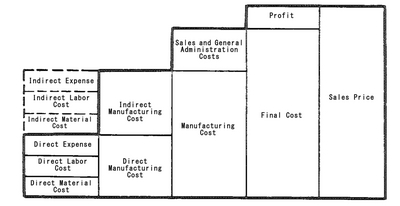

In the case of Make to Order, the sales price is generally determined by adding proper profits to the final cost (the cost used to manufacture the product and sell). In the case of Make to Stock, in contrast, the sales price is usually determined by the market price, and thus the available total cost is the remainder obtained by subtracting proper profits from the sales price.

Although the way of thinking of cost is different in between Make to Order and Make to Stock, both has the same cost structure in terms of the product sales price as shown in the figure. The product sales price is based on the manufacturing cost, which is divided into direct cost and overhead cost. The direct manufacturing cost includes direct material cost, direct labor cost, and direct expenses. By adding indirect manufacturing cost (such as utility, tool, maintenance, engineering, purchasing, and benefit costs) to the direct manufacturing cost, the manufacturing cost can be obtained. Moreover, the final cost can be obtained by adding the sales cost (such as advertisement expenses and sales persons' payment) and general administration cost to the manufacturing cost.

Although the way of thinking of cost is different in between Make to Order and Make to Stock, both has the same cost structure in terms of the product sales price as shown in the figure. The product sales price is based on the manufacturing cost, which is divided into direct cost and overhead cost. The direct manufacturing cost includes direct material cost, direct labor cost, and direct expenses. By adding indirect manufacturing cost (such as utility, tool, maintenance, engineering, purchasing, and benefit costs) to the direct manufacturing cost, the manufacturing cost can be obtained. Moreover, the final cost can be obtained by adding the sales cost (such as advertisement expenses and sales persons' payment) and general administration cost to the manufacturing cost.

Reference:JIT Business Research Mr. Hirano Hiroyuki